Europe RTD Alcoholic Beverage Market Overview - Definition, scope, and significance?

The Europe Ready‑to‑Drink (RTD) alcoholic beverage market comprises pre‑mixed drinks that combine a spirit base with mixers, flavors, and carbonation in a single, convenient package. The market covers all major European countries and includes products sold in bottles or cans through retail, on‑premise, and e‑commerce channels. Its significance lies in meeting changing consumer lifestyles that prioritize convenience, portability, and consistent quality. RTD drinks cater to both premium and mass‑market segments, offering brands an avenue to increase volume sales, reach younger demographics, and extend the lifecycle of traditional spirit portfolios.

Europe RTD Alcoholic Beverage Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for convenient alcohol solutions, the growth of premiumisation, and the expansion of e‑commerce distribution. Consumers increasingly prefer single‑serve formats that eliminate the need for mixing, especially in urban environments. A strong trend toward low‑calorie and “better‑for‑you” formulations also fuels innovation. Restraints stem from stringent alcohol advertising regulations across many European jurisdictions and higher tax rates on spirits, which can compress margins. Challenges involve supply‑chain volatility, particularly for packaging materials, and the need to differentiate in an increasingly crowded shelf space. Opportunities arise from the launch of novel flavour profiles, the integration of natural ingredients, and strategic partnerships with retail chains to secure premium shelf placement.

Europe RTD Alcoholic Beverage Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward premium spirit bases such as whiskey and gin, reflecting broader European palate preferences. Flavour experimentation—using botanicals, citrus, and exotic fruits—is gaining traction, especially in canned formats that appeal to younger, on‑the‑go consumers. Sustainability is an emerging trend; brands are adopting recyclable packaging and reduced‑sugar formulations. Additionally, limited‑edition collaborations with DJs, artists, or sports events create buzz and drive short‑term spikes in sales. The adoption of digital marketing and influencer partnerships continues to accelerate brand awareness and trial.

COVID-19 Impact on the Europe RTD Alcoholic Beverage Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted on‑premise sales as bars and restaurants closed, causing a short‑term dip in volume. However, the forced shift to home consumption accelerated the adoption of RTD products, which offered a convenient at‑home drinking experience. Recovery has been robust, with sales rebounding faster than traditional packaged spirits due to continued consumer preference for ready‑to‑drink formats. The market is now on a clear upward trajectory, supported by the lingering habit of home‑based consumption and the ongoing expansion of online grocery channels.

Europe RTD Alcoholic Beverage Market Competitive Landscape - Major competitors and market consolidation?

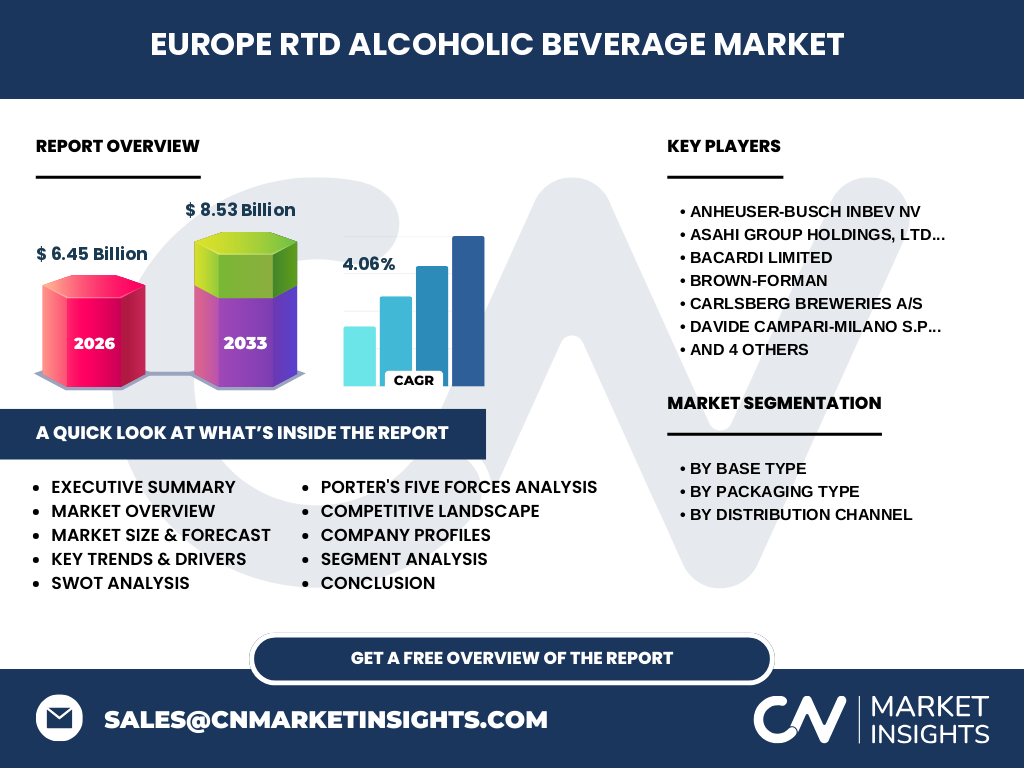

The competitive landscape is dominated by global alcohol giants that have diversified into the RTD segment. Key players include Anheuser‑Busch InBev NV, Asahi Group Holdings Ltd., Bacardi Limited, Brown‑Forman, Carlsberg Breweries A/S, Davide Campari‑Milano S.p.A., Diageo plc., Heineken N.V., Molson Coors Brewing Company, and Suntory Holdings Limited. These companies leverage extensive distribution networks and strong brand equity to capture market share. Recent years have seen strategic acquisitions of niche RTD brands and joint‑venture launches, indicating a modest level of consolidation aimed at expanding portfolio breadth and geographic reach.

Executive Summary - High-level overview and key findings about Europe RTD Alcoholic Beverage Market?

The Europe RTD alcoholic beverage market was valued at €6.45 billion in 2026 and is projected to reach €8.53 billion by 2033, representing a CAGR of 4.06 %. Growth is driven by consumer demand for convenience, premium spirit bases, and innovative flavours. Packaging trends favor both bottles and cans, with cans gaining share in on‑the‑go channels. Supermarkets and hypermarkets remain the primary distribution channel, while specialty stores provide niche premium exposure. Major multinational alcohol groups dominate the competitive arena, employing acquisitions and collaborations to strengthen their RTD foothold. The market outlook is positive, with opportunities in sustainable packaging, low‑calorie formulations, and digital engagement.

Europe RTD Alcoholic Beverage Market Forecast - Projections for 2025-2032 period?

Based on the established CAGR of 4.06 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. The forecast anticipates continued volume growth driven by premiumisation and the rising popularity of canned formats. While exact monetary values beyond 2026 are not disclosed, the projected 2027‑2033 market size of €8.53 billion underscores a robust upward momentum, suggesting that the market will outpace many traditional spirit categories in Europe.

Europe RTD Alcoholic Beverage Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by base type shows four core spirit categories: whiskey, rum, vodka, and gin. Whiskey‑based RTDs are gaining prominence due to the premium whisky trend, while gin‑based variants cater to the botanical‑flavour boom. Rum and vodka retain solid share, especially in mixed‑fruit and classic cocktail formats. By packaging type, bottles dominate the premium shelf, whereas cans are favored for on‑the‑go consumption and sustainability considerations. Distribution channels are led by supermarkets and hypermarkets, reflecting broad consumer access, with specialty stores serving as a conduit for premium and limited‑edition offerings.

Global Europe RTD Alcoholic Beverage Market Size and Share by Region - Geographic distribution?

Within the European context, the RTD alcoholic beverage market encompasses Western, Northern, Southern, and Central Europe. While specific regional monetary figures are not provided, the overall market size of €6.45 billion in 2026 reflects contributions from all major economies, with the United Kingdom, Germany, France, and Italy representing the largest consumption bases. These regions benefit from mature retail infrastructures and high disposable incomes, supporting both mass‑market and premium RTD segments.

Regional Analysis of the Europe RTD Alcoholic Beverage Market - Detailed regional market performance?

Western Europe leads in premiumisation, with consumers gravitating toward whiskey‑ and gin‑based RTDs presented in premium bottles. Northern Europe shows strong adoption of cans, driven by environmental consciousness and outdoor lifestyle preferences. Southern Europe’s market is characterised by fruit‑forward flavours, often using rum bases, aligning with local taste profiles. Central Europe exhibits balanced growth across all packaging types and base spirits, guided by a mix of price‑sensitive and premium consumers. Each sub‑region presents distinct opportunities for tailored product launches and channel strategies.

Leading Company Profiles in the Europe RTD Alcoholic Beverage Market - Industry players and strategies?

Key companies such as Diageo plc. and Bacardi Limited leverage their extensive spirit portfolios to create branded RTD extensions, capitalising on existing brand loyalty. Anheuser‑Busch InBev NV and Heineken N.V. apply their brewing expertise to develop RTD lines that complement their beer offerings, often focusing on low‑alcohol or hybrid products. Asahi Group Holdings and Suntory Holdings emphasize innovation in flavour and packaging, targeting health‑conscious consumers with lower‑sugar formulations. Brown‑Forman and Campari‑Milano pursue premium collaborations, releasing limited‑edition RTDs that highlight their flagship spirits. All players invest heavily in marketing, digital outreach, and strategic shelf‑placement to enhance visibility.

Porter's Five Forces Analysis of the Europe RTD Alcoholic Beverage Market - Competitive forces assessment?

• Threat of new entrants: Moderate. High capital requirements for brand development and distribution network creation act as barriers, though niche artisanal RTD brands can enter via specialty stores. • Bargaining power of suppliers: Low to moderate. Spirit suppliers are often owned by the same companies producing RTDs, reducing external dependency, while packaging suppliers face fluctuating material costs. • Bargaining power of buyers: High. Retail chains command significant shelf space and negotiate promotional terms, pressuring manufacturers on pricing and margin. • Threat of substitutes: Moderate. Traditional cocktails, canned beer, and non‑alcoholic ready‑to‑drink beverages compete for consumer attention. • Rivalry among existing competitors: Intense. The market is populated by large, resource‑rich firms competing on innovation, branding, and distribution, leading to frequent product launches and promotional campaigns.

SWOT Analysis of the Europe RTD Alcoholic Beverage Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong brand equity from parent spirit companies, growing consumer demand for convenience, and a diverse product portfolio across base spirits. Weaknesses: Regulatory constraints on alcohol marketing and high taxation in several countries. Opportunities: Expansion into low‑calorie and natural‑ingredient formulations, sustainable packaging innovations, and digital commerce channels. Threats: Economic downturns affecting discretionary spending, supply chain disruptions for packaging materials, and increasing competition from non‑alcoholic ready‑to‑drink alternatives.

Europe RTD Alcoholic Beverage Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw spirit production, primarily managed by major alcohol groups. Next, formulation and blending create the RTD product, followed by packaging—either bottles or cans—often sourced from third‑party suppliers. Distribution is handled through wholesale partners who deliver to supermarkets, hypermarkets, and specialty stores. The final step involves retail placement, where marketing support and shelf‑promotion drive consumer purchase. Throughout the chain, logistics and cold‑chain considerations are minimal for most RTDs, allowing efficient scaling.

Key Investment Insights in the Europe RTD Alcoholic Beverage Market - Strategic investment recommendations?

Investors should focus on companies that demonstrate a clear premium‑RTD strategy, especially those expanding whiskey and gin bases. Brands that have secured sustainable packaging commitments and low‑sugar product lines are likely to outperform regulatory scrutiny. Partnerships with leading retail chains enhance distribution leverage and margin protection. Additionally, targeting firms with strong e‑commerce capabilities will capture the accelerating online purchase behavior across Europe.

Europe RTD Alcoholic Beverage Market Conclusion - Summary and key takeaways?

The European RTD alcoholic beverage market is on a solid growth trajectory, moving from €6.45 billion in 2026 to an estimated €8.53 billion by 2033, driven by a 4.06 % CAGR. Consumer preferences for convenience, premium spirit bases, and innovative flavours underpin this expansion. While regulatory and tax environments present challenges, opportunities in sustainable packaging, health‑focused formulations, and digital distribution offer compelling pathways for growth. Major global alcohol groups dominate the space, but niche innovators can succeed through differentiated product stories and targeted channel strategies.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry executives, distributors, and retail buyers, alongside secondary data extraction from company reports, trade publications, and governmental statistics. Trend analysis was applied to historical sales data to derive the 4.06 % CAGR, which underpins the forecast. Competitive profiling leveraged publicly disclosed financials and strategic announcements of the listed key companies. All findings were validated through cross‑checking across multiple sources to ensure reliability.

Research Scope - Coverage and limitations?

The research covers the European RTD alcoholic beverage market across all major countries, focusing on the four base spirit categories, two packaging types, and three primary distribution channels. It excludes non‑alcoholic ready‑to‑drink products and does not provide granular country‑level financial breakdowns beyond the aggregated European figures. The analysis is based on data available up to 2026, with forward‑looking projections derived from the stated CAGR.

Key Companies and Recent Developments in the Europe RTD Alcoholic Beverage Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Diageo plc. recently introduced a limited‑edition whiskey‑based RTD line featuring regional botanicals, aimed at premium retail shelves. Bacardi Limited launched a rum‑centric canned RTD series targeting the summer market, emphasizing natural fruit extracts. Anheuser‑Busch InBev NV announced a partnership with a leading European supermarket chain to secure exclusive shelf space for its new vodka‑based RTD. Brown‑Forman expanded its RTD portfolio with a low‑calorie gin cocktail, leveraging its heritage branding. Campari‑Milano unveiled a collaborative RTD with a popular music festival, blending its classic aperitif with contemporary flavour twists. These initiatives illustrate the ongoing innovation and strategic alignment among the market’s leading players.